(Photo above: Getting ready for an early morning flight | Photo courtesy of David Rosell)

At the age of 12, I would often volunteer to mow my parents’ lawn since that gave me the opportunity to drive my father’s bright orange Ariens Riding Lawn Mower¬. This was the closest experience to driving a car for a raring-to-go pre-teen. I was fastidious for a kid and did my best to make the lawn look like Yankee Stadium, with precise, crisscrossed lines.

I could never have imagined that one day someone would place a 30-foot wing above a similar piece of equipment, relocate the blade behind the driver and take off down an airport runway to fly! Let alone that such a contraption would fly me high in the sky, courtesy of Fred Rafilson, Bend’s expert Ultralight pilot.

An Ultralight, also known as a flex-wing trike, is a type of powered hang glider that uses a high-performance wing coupled to a propeller-powered, three-wheeled undercarriage. The power behind last week’s ride was, yes, an Ariens riding lawn mower.

It was a sparkling morning in Central Oregon. The wind was nonexistent as we taxied down the runway at the Prineville Airport. Once we had been cleared, it took only seconds for the 50- horsepower engine to reach a speed of 32 mph. Effortlessly we took flight, our steep climb immediately offering a most spectacular view from a vantage point I had never seen before.

A Different Perspective from Above

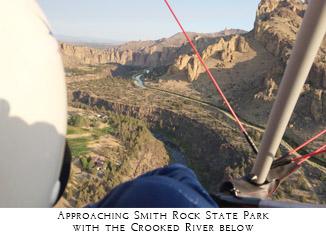

Once I eased into my new surroundings, Fred pointed out the massive Les Schwab tire warehouse and the adjacent Facebook Data Center. I spotted the Crooked River, and instantly understood how it got its name. I looked out over vast, verdant fields of alfalfa and farm houses that reminded me of Kansas.

My heart started to beat profusely as we approached Smith Rock, a sanctuary of majestic rock spires that serves as an outdoor playground to me and other rock climbing enthusiasts. As we flew adjacent to the towering walls of Phoenix Buttress, over Misery Ridge and on to Monkey Face, fears of being blown against the cliff face surfaced.

“Remain calm,” I told myself.

I knew that only by controlling my emotions and my thoughts could I help ensure a safe return.

Once we landed, I realized how completely my view of the area had changed when taking a look at my surroundings from a different perspective.

The current stock market volatility can be a very emotional time for investors. However over-investing in our emotions is bad news for our financial investments. Taking a different perspective can certainly help.

It never ceases to amaze me how violently and rapidly the market can move in both directions. Since 1946, there have been 10 bear markets where the market decline has exceeded 20 percent. The average decline has been 35 percent. When you observe the many economic challenges our country currently faces, I suggest asking yourself, “Haven’t we had some of these situations in one form or another for the past 50 years?”

Do you remember sitting in gas lines in 1973 during the oil embargo?

Do you remember when inflation rose above 13 percent in 1980?

Do you remember Black Monday in October 1987 when the U.S. stock market dropped 20 percent in one day?

What about the dot-com crash shortly after 9/11?

Then there was 2008, the worst year in stock market history.

We’ve survived these and many other financial rapids on an irregular basis for half a century. I suspect we will continue to encounter turbulent air as we pilot our way through our lifetime. The worst move one can make in the middle of such turbulence is to get tense or even bail off the Ultralight. All too often, however, that’s exactly what investors do.

Chuck Widger, the chairman of Brinker Capital, sums up my points eloquently:The flow of individual investors’ money shows that in the battle between emotions and sound strategy, emotion has taken the upper hand. Many investors abandon long-term strategies for the perceived safety of cash. This can leave a hole in your savings that never really gets repaired—you’ll always have less savings to build on than if you stayed the course. Instead of fighting an exhausting battle with your emotions, develop a diversified long-term strategy and stick to it. After all, your long-term goals don’t change overnight—so why should your portfolio?

Guidance from a Trained Instructor

Fred shared stories of how challenging it was to learn how to fly his Ultralight. “Learning was tough,” he told me. “My instructor sat behind me for over 300 landings before he was completely sure I would land safely every time. There is no margin for error. Now I feel safe to take anyone along for a ride.”

Just as Fred’s flying instructor made a significant difference when it came to learning to fly, obtaining professional investment guidance can dramatically impact your financial future and keep you from making common, costly mistakes. Benjamin Graham, a prominent economist known for coaching Warren Buffett, had the following to say when observing the irrationality during the Great Depression: “The investor’s chief problem—and even his worst enemy—is likely to be himself.”

October 19, 1987 is an ominous date known as Black Monday. It was the largest one-day percentage decline in stock market history. The Dow Jones Industrial Average (DJIA) dropped by 508 points to 1739 (22.6 percent). Investors thought the end was near and fear overtook the financial world. Interestingly, the DJIA was not only positive for the 1987 but closed on December 31st, 1987 at an all-time record high of 1,939 points.

Today, the DJIA can now fluctuate in a single trading day by as much as Black Monday’s 508 points. If someone had told you back then that in 2015 the DJIA would surpass 18,000, you would have thought they had lost their sensesThe economy will more than likely continue its yo-yo-like movements. Obtaining guidance from a financial advisor can help you live the life you have imagined in your years of retirement despite those ups and downs.

Do You Have a Parachute for your Investments?

Fred tells me that the Ultralights are extremely safe. Even so, he built in a Ballistic Recovery System just in case of a catastrophic event.

“I pull the handle and BANG, the rocket fires instantaneously, pulling the chute out and away from the trike. Once inflated, it brings the trike and passengers safely to the ground,” he explained. “You’ll probably will never need it, but it’s good insurance!”

Wouldn’t it be great if there was a type of portfolio insurance that enabled you to stay invested in the market while providing guarantees that you would have an income stream for life regardless of market performance? These benefits are now available. When used appropriately for the right people, for the right portion of a portfolio, and at the right time in your life, they can save that retirement income you’ve worked most of your life to accumulate. You probably insure your most valuable assets, including your home, cars and boat. Now it’s possible to insure what for most people at or near retirement is their most valuable financial asset: your retirement accounts.

Think of an annuity as the opposite of life insurance. Life insurance is meant to protect loved ones should you die prematurely. Annuities are there to protect you, should you outlive your retirement savings.

Today, the modern-day Variable Annuity (VA) with living benefits offers a compelling scenario. In July 2009, The Wall Street Journal ran a story titled “Long Derided This Investment Now Looks Wise—Thanks to Guarantees, Variable Annuities Paid When Stock Didn’t.” The headline says it all. Variable Annuities can ease investors’ anxieties and lead to better investment outcomes.

In the past, retired investors debating about whether to get out of the market or stay in have faced a make-or-break decision. By electing to put the money into a VA with a living benefit, this decision is no longer an issue. These VA investors are now protected against the market’s downside because they have guaranteed lifetime income throughout their retirement.

VAs, like any investment strategy, should be only part of the retirement security puzzle. Just keep in mind that this investment strategy can mitigate both our worst knee-jerk reactions and underperforming markets, while offering investors the guarantees and psychological support needed to maintain market exposure. There is no greater value than peace of mind when it comes to your investments, especially during your retirement years.

David Rosell is President of Rosell Wealth Management in Bend. www.RosellWealthManagement.com. He is the author of Failure is Not an Option- Creating Certainty in the Uncertainty of Retirement. You may learn more about his book at www.DavidRosell.com or Amazon.com. Ask for David’s book at Barnes & Noble, Newport Market, Cafe Sintra, Bluebird Coffee Shop, Dudley’s Bookshop and Powell’s Books in Portland.

Investment advisory services offered through Rosell Wealth Management, a State Registered Investment Advisor. Securities offered through ValMark Securities, Inc. Member FINRA, SIPC 130 Springside Drive, Ste 300 Akron, Ohio 44333-2431. 800-765-5201. Rosell Wealth Management is a separate entity from ValMark Securities.